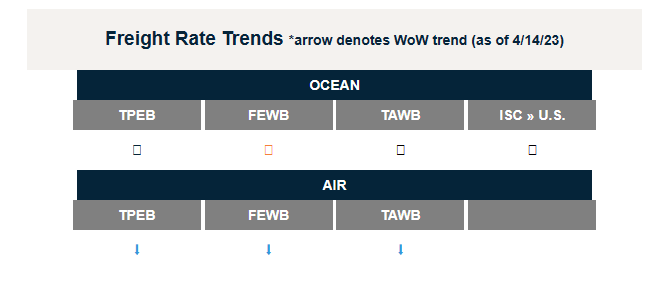

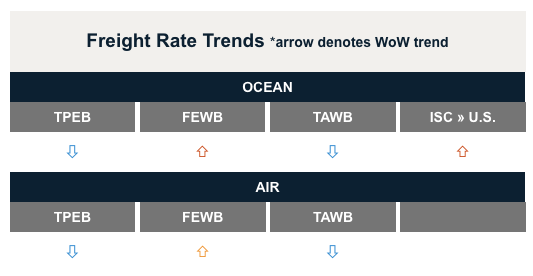

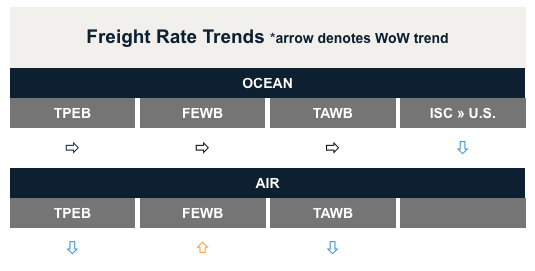

Ocean Freight Market Update

Asia → North America (TPEB)

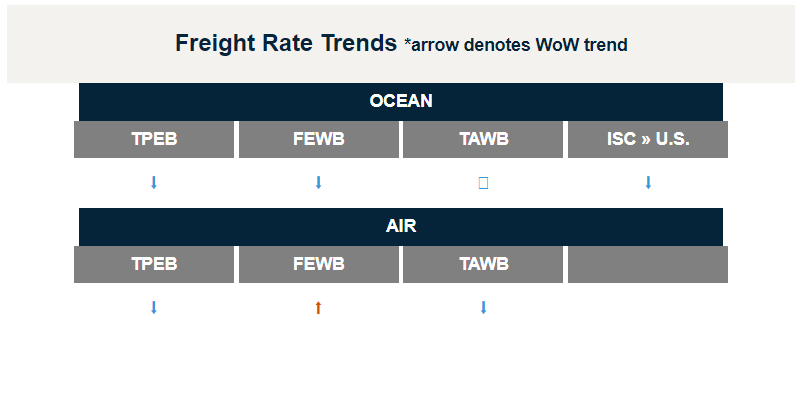

- Transpacific Eastbound (TPEB) Carriers look to pick up rate slack amid low volume market.

- U.S.: Current TPEB market capacity and demand levels look to hold through the end of March. Prospects of general rate increases (GRI) for April 1st appear more common from the carriers than in previous months. Routine blank sailings on almost all tradelanes will persist through the end of March, as well.

- Canada: Market and rate conditions are similar to the U.S. Vancouver continues to see stable vessel dwell counts (1 vessel) as well as berthing delays (3 days, 9 days for rail dwell).

- Rates: Soft on most origin-destination combinations.

- Space: Open.

- Capacity/Equipment: Open.

- Recommendation: Book at least 2 weeks prior to cargo ready date (CRD), and keep upcoming blank sailings in mind.

Asia → Europe (FEWB)

- Demand and Supply are a bit more balanced this week after the blank sailings seen immediately following Lunar New Year (LNY). Booking intake is gradually improving but still not as strong as pre-LNY. Rates are still under pressure.

- Rates: Generally reduced or extended for the first half of March.

- Capacity/Equipment: Still seeing around 10-20% blank sailing average in weeks 11/12/13 to adjust for the decrease in demand. Expect the carriers to continue the same trend into March.

- Recommendation: Allow flexibility when planning your shipments due to anticipated congestion and delays (rolls).

Europe → North America (TAWB)

- Demand remains low and space continues to be widely available. Capacity is still outstripping demand and we expect this to continue for the foreseeable future.

- Rates: The drop continues as demand is not picking up at the same pace as last year and vessel utilization is in the 65-70% range, down from 90% a few months ago.

- Space: Due to the easing of congestion, space into the U.S. East Coast (USEC) and U.S. West Coast (USWC) is coming online.

- Capacity/Equipment: Equipment availability keeps getting better as congestion disappears. Low empty stacks at inland depots are also getting better in some areas, but prioritize pick-up from the Port of Loading if possible.

- Recommendation: Book 2-3 or more weeks prior to CRD. Request premium service for higher reliability and no-roll.

Indian Subcontinent → North America

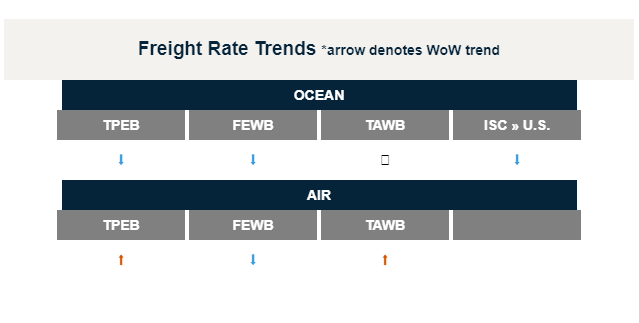

- An increase in rates is expected as carriers announce General Rate Increases (GRIs) for the end of March and April. Full implementation of these GRIs is not expected, but slight increases will be felt across most Ports of Loading (POLs).

- Rates: Remain from 1H March.

- Space: Open.

- Capacity/Equipment: Slight capacity constraints to USWC. Equipment remains top of mind, but varies drastically based on carrier, POL, and equipment type.

- Recommendation: Be open to procuring equipment from wet ports vs. inland container depots and to use alternative services that may be slightly more expensive, but with less service disruptions.

North America → Asia

- Capacity is available across all major services, and carriers are looking for volume opportunities. No major services to the Asia Pacific (APAC) region are seeing space constraints.

- Congestion has been cleared out across most North American container yards with improved operations as a result of lowered demand.

- Equipment is available and ample in most major markets.

- The outlook at the end of Q1 and headed into Q2 is that most of the existing capacity will remain in place as carriers lightly reshuffle vessel capacity across trades.

- Rates: Rate pressures continue the trend slightly downwards MoM on certain lanes from coastal ports to Asia base ports. All carriers are trying to push cargo onto these lanes/services. Deals below existing market levels are available for consistent volume opportunities.

- Space: Very open, allocation requests can be made to carriers for high volume weeks or projects with a high probability of acceptance.

- Capacity/Equipment: no major capacity changes in the market. No major equipment hurdles to highlight. The only pocket shippers should monitor are IPI’s where chassis availability may be low.

- Recommendation: book 1-2 weeks prior to CRD on all coastal to Asia-based port lanes, and book 2-3 weeks prior to CRD on all inland to Asia and feeder port lanes.

North America → Europe

- Capacity from the USEC is available, while certain services from the USWC and Gulf remain tight but stable.

- Most USEC to N. Europe (NEU) and Mediterranean (MED) services have low capacity utilization levels with no space constraints.

- Gulf Coast to NEU and MED services continue to have medium to high utilization levels as the market has seen a reintroduction of capacity. Still there are some inconsistencies in the schedules from the Gulf.

- The USWC to NEU, MED services are still limited in options and therefore utilization levels are artificially high.

- Rates: Rates trended slightly downward QoQ on USEC to NEU lanes. Carriers made adjustments early in Q1 and since then rates have remained flat. Gulf and USWC rates were not adjusted in Q1 given the utilization levels on those services. Carriers are willing to make deals for USEC opportunities.

- Space: Space is open from USEC, manageable from Gulf, and limited from USWC.

- Capacity/Equipment: no major capacity changes in the market. No major equipment hurdles to highlight in the US, save for pockets of potential chassis issues out of IPI’s.

- Recommendation: book 2 weeks prior to CRD on all EC to NEU, MED lanes, book 3 weeks prior to CRD on all Gulf to NEU, MED lanes, book 4 weeks prior to CRD for all PSW to NEU lanes.

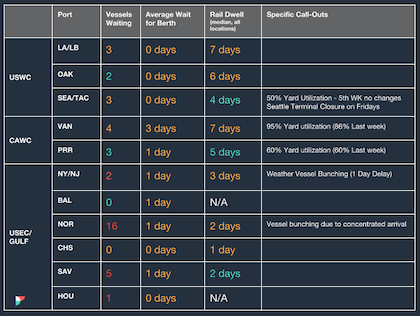

North America Vessel Dwell Times

Air Freight Market Update

Asia

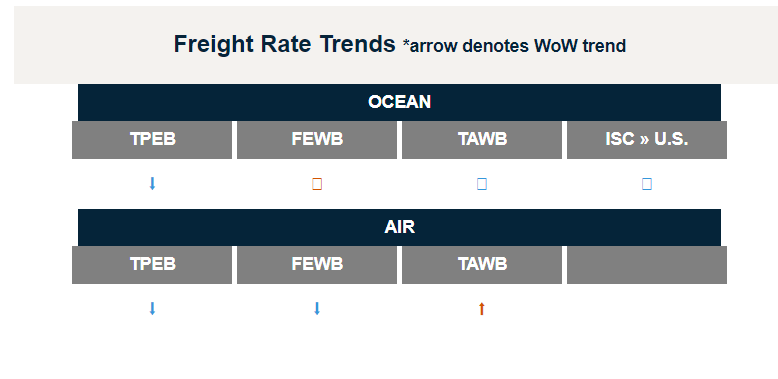

- N. China: TPEB demand has decreased this week with rates also lowering as well. The FEWB market is showing an opposite trend with both demand and rates increasing from the week prior.

- S. China: TPEB supply is tight with demand increasing in the market, resulting in rates increasing from the week prior. The Far East Westbound (FEWB) market is following at a similar trend but at a slower pace. As demand increases, expect longer booking times at origin.

- Taiwan: The market is picking up as we approach the quarter end. Rates are increasing while capacity is getting tighter.

- Korea: Rates remain the same as the previous week with no large increases in market demand.

- SE Asia: Quarter-end TPEB demand in northern Asia is causing rates to increase and hub capacity to tighten. The FEWB market remains stable.

Europe

- TAWB demand continues to fluctuate between point pairs Ex EU and UK, this is reflected in the rate levels increasing and decreasing week over week.

- There is sufficient capacity available in the market, however, expect longer lead days for direct routing. Where possible indirect options via secondary hubs are providing shorter lead days and better rates.

- No operational disruptions reported in EU & UK.

- For all lanes: Continue to place bookings early to secure best uplift options/routings. If the lead time can take a deferred option via a secondary hub, bookings could benefit from lower rate levels.

Americas

- Export demand remains steady from all markets.

- US airports are running at a normal pace.

- Capacity is opening up further, especially into Europe.

- Rates remain stable week over week.

Trucking & Intermodal

Europe

- Inland waterway shipping, or in short barging, is becoming more and more the transport modality of choice for moving containers from the Rotterdam Ocean Port to the ‘Hinterland’, not only into the Netherlands but also cross border to Germany and Switzerland.

- There is an expectation that container transport to and from the main port of Rotterdam will grow significantly over the next 20 years. If this growth is accommodated by road transport, our roads will become completely blocked. There is a lot of unused capacity in the system of inland waterways and inland shipping is capable of transporting large volumes. Compared to transport by lorry or plane, inland shipping produces far less CO2. Moreover, inland shipping accidents are rare.

Americas

Import/Export Market Trends

- Congestion is improving at Canadian ports and rail ramps, there are no significant operational delays.

- CP Vaughan Intermodal Terminal is an exception where truckers, at time, are still experiencing 4-6 hours of waiting time.

- CN continues shuttling containers from Brampton terminal to the CN Misc terminal, charging $300 per container.

- Memphis, Houston, Detroit, Savannah, and Oakland are seeing some delays and import dwells > 10 days.

- The port of Houston will be discontinuing Saturday operations at Bayport + Barbours cut on April 29th.

- Congestion fees will no longer be active, effective March 1.

- Majority of US ports and rail ramps are fluid, and not experiencing any significant delays.

- Highway Diesel have remained relatively stable YTD.

US Domestic Trucking Market Trends

- The FreightWaves SONAR Outbound Tender Volume Index (OTVI), which measures contract tender volumes across all modes, was down 25% year-over-year (3.3% month-over-month), or 9.6% when measuring accepted volumes after the significant decline in tender rejection rates. ‘

- In addition to this, the Cass report indicated year-over-year volumes were down 3.9% in December after falling 3.3% month-over-month from November. This trend illustrates shipment volumes are declining compared to last year, but much more gradually.

- The Morgan Stanley Dry Van Freight Index is another measure of relative supply; the higher the index, the tighter the market conditions.

- Throughout December, trends closely followed this curve, indicating that market pressures were consistent with average historical trends. Looking forward, we expect to see softening through at least February as seasonal demand eases in the first two months of the year.

Customs and Compliance News

Next COAC Meeting Scheduled

CBP’s Commercial Customs Operations Advisory Committee (COAC) will next meet March 29, 2023 in Seattle, CBP said in a notice. The trade community can submit comments, which are due in writing by March 24, 2023.

UFLPA Interactive Dashboard Announced

On March 14, 2023, Acting CBP Commissioner Troy Miller announced a new Uyghur Forced Labor Prevention Act (UFLPA) interactive dashboard. The statistics provided on this dashboard include shipments subject to UFLPA reviews or enforcement actions. This dashboard shows the commodity type found in detained shipments and their country of origin.

Freight Market News

Maersk Returns to Ukraine With Container-on-Barge Service

After ceasing operations in Ukraine, Maersk announced a return to service via freshwater ports along the Danube estuary in the northern part of the country. The shallow-draft terminals have operated relatively smoothly throughout the year, so Maersk has implemented container-on-barge services via the Constanta/Danube Channel and the Black Sea with a transit time of approximately a day and a half.

Source from Flexport.com